If you’ve taken out an Economic Injury Disaster Loan (EIDL), there’s a good chance you’ve come across a requirement for hazard insurance. For many business owners, this isn’t something they expected, and naturally, it raises a few questions. What exactly does it mean? Why is it required? And perhaps more importantly, what could happen if you don’t have it in place?

The truth is, hazard insurance for EIDL loan compliance is not as complicated as it may seem at first. Once you understand how it works and why it exists, it becomes much easier to handle—and even more importantly, easier to manage proactively instead of reacting to notices later on.

What Is Hazard Insurance in Simple Terms?

At its core, hazard insurance is designed to protect physical business property from damage caused by specific risks. These risks often include events like fire, storms, or other types of accidental damage.

In the context of an EIDL loan, this coverage is tied to the assets that are used as collateral. So, if your business equipment, inventory, or property is part of what secures the loan, hazard insurance ensures that those assets are protected if something unexpected happens.

It’s worth noting that hazard insurance is not the same as general business insurance. While some policies may overlap, this type of coverage is specifically focused on physical damage to tangible assets, not liability or operational risks.

Why the SBA Requires Hazard Insurance

The requirement for hazard insurance exists primarily to protect the value of the collateral tied to your loan. When a loan is secured by business assets, those assets represent a form of security for the lender.

If those assets are damaged or destroyed and there’s no insurance in place, the financial risk increases significantly. Because of that, the SBA includes hazard insurance as part of the loan conditions.

At the same time, this requirement isn’t just about the lender. From a business standpoint, it also acts as a safeguard. Instead of absorbing a full loss, you have coverage that helps you recover more smoothly.

When Hazard Insurance Becomes Necessary

Not all EIDL borrowers are expected to have hazard insurance in place immediately. However, the requirement typically comes into play when the loan exceeds a certain amount.

In most cases:

- Loans above $25,000 involve collateral

- Once collateral is involved, hazard insurance is expected

Even so, timing can vary. Some borrowers are asked to provide proof later in the process. Because of that, it’s smart to understand the requirement early rather than waiting until you’re asked for documentation.

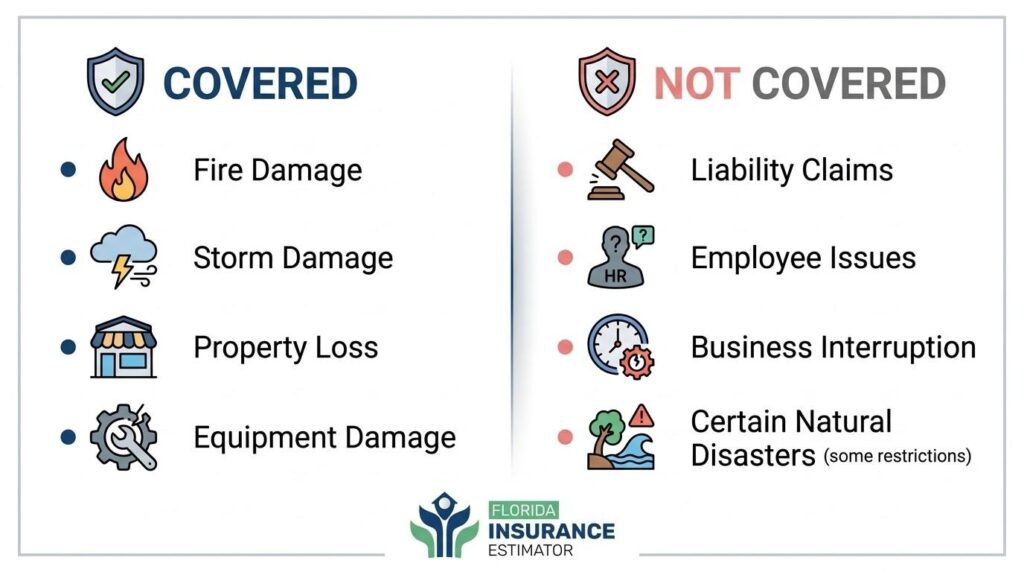

What Hazard Insurance Usually Covers

Hazard insurance focuses on protecting physical assets from specific types of damage. While policies can differ, coverage generally includes:

- Fire and smoke damage

- Storm-related damage (depending on policy terms)

- Vandalism or theft in certain situations

- Damage to business property and equipment

- Loss of inventory due to covered events

That said, it’s equally important to understand what falls outside this coverage.

Hazard insurance typically does not include:

- Liability protection

- Employee-related incidents

- Loss of income from business interruption

- Certain natural disasters unless added separately

Because of these limitations, many businesses combine hazard insurance with other types of coverage to create a more complete protection plan.

How Much Coverage Is Considered Enough?

A question that often comes up is how much coverage is actually sufficient.

In general, the SBA expects your insurance to reflect the value of the assets tied to the loan. That means your policy should be strong enough to repair or replace those assets if they are damaged.

If the coverage is too low, it may not meet the requirement. On the other hand, excessive coverage may not be necessary either.

For businesses trying to get a better sense of property-related coverage, tools like an FL insurance estimator can offer a useful starting point before speaking with an insurance provider.

What Could Happen If You Don’t Have Hazard Insurance?

This is one area where many borrowers feel uncertain.

If hazard insurance is required and not maintained, it can lead to compliance issues with your loan. Initially, you may receive reminders or requests for proof of coverage. However, if the requirement continues to go unmet, it could lead to more serious concerns tied to your loan agreement.

While it doesn’t always escalate immediately, ignoring it is not a good idea. Addressing it early tends to be much easier than dealing with it later under pressure.

How to Get Hazard Insurance

The process of getting hazard insurance is usually straightforward.

You can:

- Contact your current insurance provider

- Update your existing business policy

- Purchase a separate policy if needed

When reviewing your options, make sure:

- Your business assets are clearly covered

- Coverage limits align with asset value

- The policy meets SBA expectations

Also, keep your documentation organized. If proof is requested, having everything ready will save time and avoid unnecessary delays.

Common Mistakes to Watch Out For

Even though the requirement is fairly simple, a few common mistakes can cause problems.

Assuming Any Insurance Is Enough

Not all policies include hazard coverage. Always double-check.

Choosing Coverage That’s Too Low

Underinsuring assets can lead to compliance issues.

Waiting Until the Last Minute

Delays can create unnecessary stress and rushed decisions.

Not Reviewing Policy Details

Understanding what’s included—and what isn’t—makes a big difference.

Avoiding these mistakes helps ensure everything stays smooth and compliant.

How This Fits Into Your Overall Business Strategy

While hazard insurance is tied to your EIDL loan, it also plays a bigger role in protecting your business.

Unexpected events are part of running any business. When they happen, having the right coverage in place can make recovery much more manageable.

Because of that, hazard insurance shouldn’t be seen as just a requirement. It’s part of a broader approach to risk management and long-term stability.

Final Thoughts

Understanding hazard insurance for EIDL loan requirements doesn’t have to feel overwhelming. Once you break it down, it comes down to a few key things:

- Protecting your business assets

- Meeting your loan obligations

- Being prepared for unexpected events

The most important thing is to stay proactive. When you understand what’s required and take action early, the process becomes much simpler—and far less stressful.

In the end, it’s not just about compliance. It’s about making sure your business is protected in a way that supports long-term growth and stability.