Introduction

Severe storms can cause significant damage to a home’s roof. High winds, heavy rain, hail, and flying debris often leave homeowners dealing with leaks, missing shingles, or structural issues. In these situations, filing a roof damage insurance claim can help cover repair costs. However, many homeowners are unsure how the process works or how to improve the chances of getting their claim approved quickly.

Understanding the claims process, preparing proper documentation, and communicating clearly with your insurance provider can make a major difference. The following tips explain how to approach a storm-related roof claim in a practical and informed way.

Understand What Your Insurance Policy Covers

Before filing a claim, it is important to review your homeowners insurance policy. Coverage for storm damage varies depending on the type of policy and the cause of the damage. In many cases, roof damage insurance covers problems caused by sudden events such as hailstorms, wind damage, or fallen branches.

However, insurance typically does not cover damage caused by normal wear and tear, poor maintenance, or aging materials. Because of this, understanding the terms of your policy can help set realistic expectations before submitting an insurance claim on roof repairs.

If any part of the policy is unclear, homeowners should contact their insurer or review the policy documentation carefully.

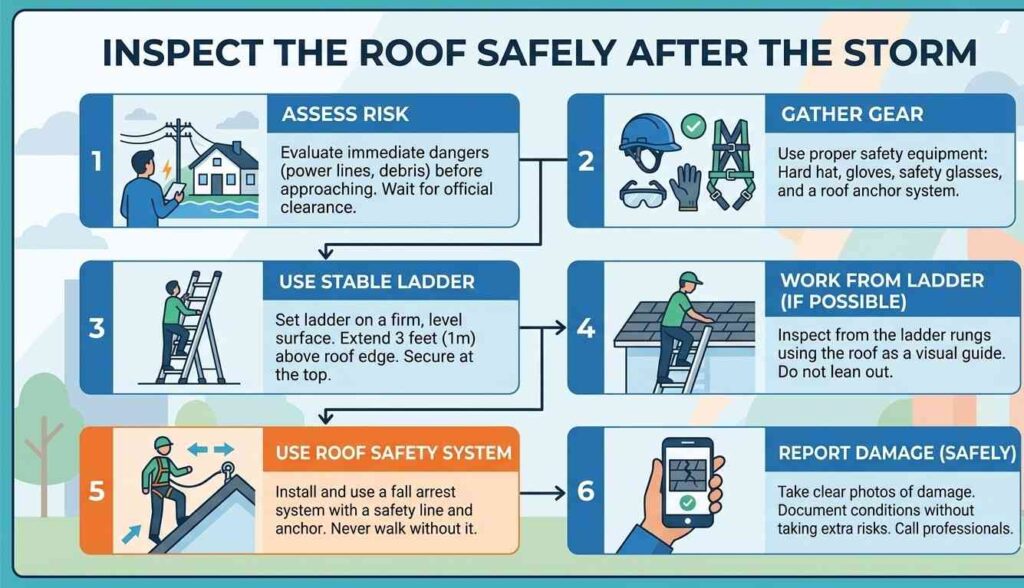

Inspect the Roof Safely After the Storm

After a storm passes, homeowners should inspect their property for visible damage. Missing shingles, dented flashing, debris accumulation, and water leaks inside the home can all indicate roof damage.

Safety should always come first. Instead of climbing onto the roof immediately, begin by checking the ground around the home for fallen materials or broken shingles. Photos taken from the ground or from a safe vantage point can provide useful documentation when preparing a roof damage claim.

If damage appears significant, contacting a professional roofing contractor for an inspection can provide a more detailed assessment.

Document the Damage Thoroughly

Accurate documentation is one of the most important steps when filing a roof damage insurance claim. Insurance companies rely heavily on evidence to determine whether the damage qualifies for coverage.

Helpful documentation may include:

- Clear photographs of damaged shingles, flashing, or gutters

- Pictures showing debris or storm impact around the property

- Notes describing when the storm occurred and when damage was discovered

- Inspection reports from roofing professionals

Organizing this information before contacting the insurer helps streamline the claims process and reduces delays during evaluation.

Report the Damage Promptly

Timing plays a major role in how smoothly an insurance claim roof request is processed. Many policies require homeowners to report storm damage within a specific timeframe.

Submitting the claim soon after the storm helps demonstrate that the damage resulted from the event rather than from gradual deterioration. In addition, early reporting allows insurance adjusters to inspect the property while evidence is still visible.

Delaying a claim could lead to complications, especially if additional weather events occur after the initial storm.

Work With the Insurance Adjuster

Once the claim is submitted, the insurance company usually sends an adjuster to evaluate the roof. The adjuster’s job is to determine the extent of the damage and estimate repair costs.

During this inspection, homeowners should be prepared to:

- Share documentation and photographs

- Provide details about the storm event

- Answer questions about when the damage was discovered

Clear communication helps the adjuster understand the situation accurately. In many cases, the adjuster’s report plays a key role in determining whether the roof claim will be approved.

Avoid Temporary Fixes That Hide Damage

Homeowners often want to protect their property immediately after a storm. Temporary measures such as covering exposed areas with tarps can prevent further water damage.

However, permanent repairs should not be completed before the insurance adjuster has inspected the roof. Making major changes too early could make it difficult to verify the original damage.

Instead, focus on temporary protective steps that prevent additional harm while still allowing the adjuster to see the affected areas.

Consider Long-Term Roof Replacement Factors

Sometimes homeowners wonder whether they should mention recent roof upgrades when filing a claim. A common question is should I tell insurance about new roof installations or improvements.

In general, transparency is important. Informing the insurance provider about a recently installed roof may help demonstrate that the damage is related to the storm rather than to age or deterioration.

Additionally, newer roofing materials may affect how the insurance company calculates replacement costs or depreciation.

Plan Your Budget While Waiting for Claim Approval

Roof repair or replacement can be costly, and insurance claims may take time to process. While waiting for approval, homeowners often review their financial options and overall housing costs.

Understanding monthly expenses, including mortgage payments and home repairs, can help homeowners plan ahead. Tools like a home loan estimator can provide a broader view of housing-related financial commitments when unexpected repairs arise.

Although insurance may cover part of the repair costs, budgeting for potential out-of-pocket expenses is still a practical step.

Follow Up on the Claim Status

After the adjuster completes the inspection, the insurance company reviews the report and determines the claim outcome. This process can take time depending on the insurer and the complexity of the damage.

If homeowners do not receive updates within the expected timeframe, it is reasonable to follow up with the insurer. Keeping communication professional and organized helps ensure the claim remains active and properly documented.

Maintaining copies of emails, claim numbers, and inspection reports can also make future discussions easier.

Final Thoughts

Storm damage can be stressful, especially when it affects something as essential as a home’s roof. Filing a roof damage insurance claim requires patience, accurate documentation, and a clear understanding of the insurance process.

By inspecting the property safely, documenting the damage thoroughly, and communicating promptly with the insurance company, homeowners can improve their chances of receiving faster claim approval. Most importantly, taking a thoughtful and informed approach ensures that the claims process remains focused on protecting the home and restoring safety after severe weather events.