Introduction

Buying a home is one of the biggest financial step most people take. Protecting that investment with the right homeowners insurance is equally important. Yet many homeowners select a policy based only on price, without fully understanding what their coverage includes or excludes. The right policy should do more than meet lender requirements—it should provide reliable protection for your home, belongings, and financial security.

If you’re in the process of choosing the right homeowners insurance, the following tips can help you make a well-informed decision.

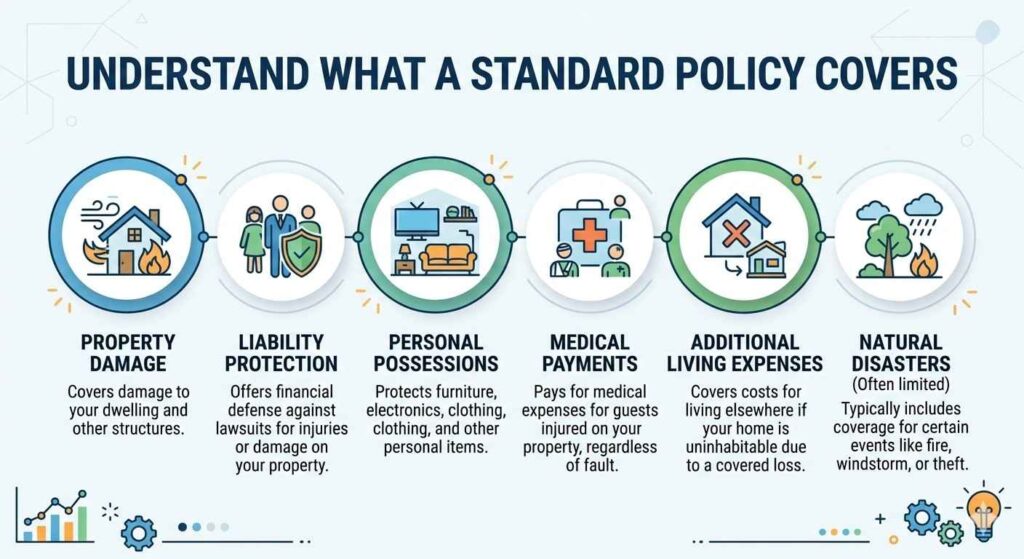

Understand What a Standard Policy Covers

Before comparing insurers, it’s important to understand the basics of a homeowners insurance policy. Most standard policies provide several types of protection, including:

- Dwelling coverage, which helps cover damage to the home’s structural components.

- Personal property coverage for belongings such as furniture, electronics, and clothing

- Liability protection in case someone is injured on your property

- Help with short-term living expenses when damage makes your home unlivable

However, not every type of damage is included. For example, many policies exclude floods or earthquakes, which may require separate coverage. Reviewing policy details carefully helps ensure you know exactly what risks are protected, Reviewing this information can make it easier to understand homeowners insurance coverage before selecting a policy.

Calculate the True Replacement Cost of Your Home

One of the most common mistakes homeowners make is confusing market value with replacement cost. Replacement cost refers to how much it would take to rebuild your home from the ground up using current construction prices.

If your coverage limit is too low, you could face significant out-of-pocket costs after a major loss such as a fire or severe storm. When evaluating policies, ask your insurer how they estimate rebuilding costs and whether your policy includes replacement cost coverage or actual cash value. The former typically provides better financial protection because it does not deduct depreciation.

When planning for homeownership expenses, insurance is only one part of the bigger financial picture. Understanding how your mortgage payments, property taxes, and insurance premiums fit into your monthly budget can help you make smarter decisions. If you’re evaluating overall housing affordability, using a home loan estimator can provide a clearer view of potential loan payments and long-term costs before committing to a policy or property purchase.

Compare Multiple Insurance Providers

Insurance pricing and coverage options can vary widely between providers. Getting quotes from several reputable insurers allows you to evaluate both the cost and the policy terms.

While price is important, it should not be the only factor. Consider elements such as:

- The company’s reputation and financial strength

- Customer satisfaction ratings

- Claims handling process and response time

- Coverage options and flexibility

A slightly higher premium may be worth it if the insurer offers better support and reliability during the claims process.

Evaluate Deductibles and Policy Limits

A deductible is the portion of a claim you must cover yourself before the insurer pays the remaining costs. Policies with higher deductibles typically have lower monthly premiums, while lower deductibles often increase premium costs.

When choosing a deductible, think about what you could realistically afford in the event of a claim. The goal is to strike a balance between manageable monthly payments and financial readiness for unexpected damage.

Additionally, review coverage limits for personal belongings, liability protection, and other components of your policy. Adjusting these limits may help ensure your coverage aligns with your real needs.

Look for Discounts and Bundling Opportunities

Many insurers offer ways to reduce premiums without sacrificing coverage. Common discounts may include:

- Bundling homeowners insurance with auto insurance

- Installing home security systems or smoke detectors

- Maintaining a claims-free history

- Upgrading roofing or electrical systems

These incentives can make a meaningful difference in long-term insurance costs. It’s always worth asking insurers about available discounts when comparing policies.

Review the Policy Details Carefully

Insurance policies contain specific conditions, exclusions, and limitations that may not be obvious at first glance. Taking the time to review policy language can prevent misunderstandings later.

Pay particular attention to:

- Coverage exclusions

- Policy limits that apply to expensive items such as jewelry and collectibles.

- Optional add-ons or endorsements

- The claims process and documentation requirements

If anything is unclear, ask your insurance agent or provider to explain it in detail. Understanding your policy now can save significant stress during an unexpected situation.

Making a Confident Insurance Decision

Choosing the right homeowners insurance requires careful consideration of coverage, costs, and long-term protection. While it may seem complex at first, focusing on the fundamentals—coverage types, replacement value, insurer reliability, and policy terms—can simplify the process.

A well-chosen insurance policy provides more than financial protection; it offers peace of mind. With the right coverage in place, homeowners can feel confident that their property, belongings, and financial future are better protected against unexpected events.

By approaching and choosing the right homeowners insurance with research and thoughtful planning, you can select a policy that truly supports your needs today and in the years ahead.