Introduction

Florida’s insurance market is unique. Because the state regularly faces hurricanes, flooding, and other natural disasters, insurers must manage extremely high levels of risk. One of the most important tools they use to stay financially stable is reinsurance.

But what exactly is it, and why does it matter for homeowners in Florida? Below are common questions and clear answers to help explain the concept and its impact on the insurance industry.

What Is Reinsurance?

It is a form of insurance that insurance companies purchase to protect themselves from large financial losses. In simple terms, it allows an insurance company to transfer part of its risk to another insurer known as a reinsurer.

When an insurance company sells homeowners policies, it takes on the responsibility of paying claims if a disaster occurs. However, if a major event such as a hurricane causes thousands of claims at once, the financial burden could be overwhelming. Reinsurance spreads that risk across multiple companies so that one insurer is not solely responsible for massive losses.

Understanding what re-insurance in insurance helps explain why it plays such an important role in protecting the overall stability of the insurance market.

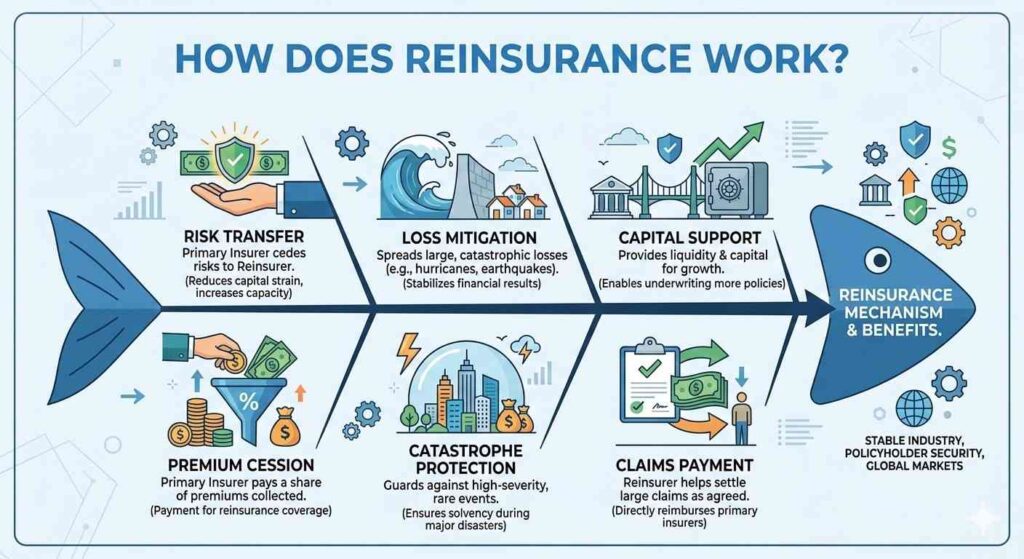

How Does Reinsurance Work?

To understand how does reinsurance work, imagine a simple example. A Florida insurance company sells thousands of homeowners policies along the coast. Because the area is vulnerable to hurricanes, the insurer knows a major storm could generate billions of dollars in claims.

To reduce that exposure, the insurer purchases from a larger global reinsurer. In exchange for a premium, the reinsurer agrees to cover a portion of the losses if claims exceed a certain threshold.

For instance, the agreement may state that the reinsurer will pay claims after the insurer’s losses reach a specific level. This arrangement helps insurers remain solvent after catastrophic events while still offering coverage to homeowners.

In practice, several reinsurers may share the same risk, distributing potential losses across multiple companies worldwide.

If you want to learn more about how insurance companies manage risk and maintain financial stability, independent regulatory organizations provide useful educational resources. The National Association of Insurance Commissioners offers consumer guidance on insurance risk management and coverage basics, helping policyholders better understand how insurers protect themselves from large losses.

Why Is Reinsurance Especially Important in Florida?

Florida’s geographic location makes it one of the most disaster-prone regions in the United States. Hurricanes, severe storms, and flooding create a high concentration of risk for property insurers.

Because of this environment, local insurers rely heavily on it to remain financially stable. Without it, many companies would struggle to afford the cost of large-scale claims after a major storm season.

it helps make to possible for insurers to continue offering policies to Florida residents. It also allows companies to manage risk more effectively while maintaining adequate financial reserves.

Does Reinsurance Affect Homeowners Insurance Rates?

Yes, reinsurance can influence the cost of homeowners insurance.

When insurers purchase reinsurance protection, they pay significant premiums to reinsurers. Those costs are often reflected in the pricing of insurance policies. If global reinsurance prices increase—often after major disasters—insurance companies may raise premiums to offset the higher costs.

This is one reason why homeowners in hurricane-prone areas sometimes see insurance prices fluctuate after severe storm seasons. While it may not be the only factor affecting rates, reinsurance plays a major role in shaping the overall cost structure of the market.

What Types of Reinsurance Do Insurers Use?

Insurance companies typically rely on several types of reinsurance agreements depending on their risk management strategy.

One common structure is proportional reinsurance, where the reinsurer shares both the premiums and the claims with the primary insurer. Another approach is excess-of-loss reinsurance, where the reinsurer only pays once losses exceed a predetermined level.

These arrangements allow insurers to tailor their risk protection based on their portfolio, geographic exposure, and financial capacity.

How Does Reinsurance Support Market Stability?

Beyond protecting individual insurers, reinsurance contributes to the stability of the entire insurance market.

When catastrophic events occur, reinsurers absorb a portion of the financial impact. This prevents large-scale insurer failures and helps ensure that policyholders continue to receive claim payments.

Reinsurance also enables smaller regional insurers to compete in markets like Florida by providing additional financial backing. Without this support, many companies would not be able to offer coverage in high-risk areas.

Why Should Homeowners Understand Reinsurance?

Although homeowners never purchase reinsurance directly, it still affects them in several ways.

It influences how insurance companies price policies, how much coverage insurers can offer, and how resilient the industry remains after disasters. By understanding the basics of reinsurance, homeowners can better interpret changes in the insurance market and policy pricing.

In states like Florida—where natural disasters are a constant concern—the role of reinsurance becomes even more significant.

Final Thoughts

Understanding what is reinsurance helps reveal an important part of how the insurance industry manages risk. By sharing potential losses with reinsurers, insurance companies can protect themselves from catastrophic financial events and continue serving policyholders.

For Florida’s insurance market, reinsurance is not just a financial tool—it is a critical component that allows insurers to operate in a high-risk environment while maintaining stability for homeowners and communities alike.