Introduction

Understanding the difference between home warranty vs home insurance is less about definitions and more about recognizing how risk actually works in a home.

Every property faces two ongoing realities. First, there are sudden, unpredictable events—storms, fires, or accidents. Second, there is gradual decline—systems wear out, appliances fail, and performance drops over time. While both situations can be costly, they are treated very differently in terms of coverage.

Because of this, homeowners who assume one solution covers everything often find themselves unprepared at the worst possible moment. So, to make a well-informed decision, it’s important to understand exactly where each type of protection begins—and where it ends.

The Core Difference Most People Overlook

At a surface level, both home warranties and home insurance offer financial protection. However, the trigger behind that protection is entirely different.

Home insurance responds to events.

A home warranty responds to conditions.

In other words, insurance is activated when something unexpected happens. Meanwhile, a warranty applies when something simply stops working as it should.

This distinction may seem subtle at first. However, it ultimately determines whether a claim is approved or denied.

How Home Insurance Works in Real Terms

Home insurance is structured to protect against sudden and external damage. These are situations that are not only unplanned but also often severe in financial impact.

What It Typically Covers

A standard homeowners policy usually includes:

- Structural damage caused by fire, storms, or vandalism

- Loss or damage to personal belongings

- Coverage that helps protect you financially if a person gets hurt while on your property

- Temporary housing costs if your home becomes unlivable

For instance, if a severe storm damages your roof or a fire spreads through part of your home, insurance is designed to step in and absorb much of that financial burden.

However, just as important as what is covered is what is not.

Where Home Insurance Stops

Home insurance generally does not apply to:

- Mechanical failures

- Aging systems

- Routine maintenance issues

So, if your HVAC system stops working after years of use, that situation would fall outside the scope of insurance coverage.

What a Home Warranty Actually Covers

This is where a home warranty becomes relevant.

Rather than focusing on disasters, a home warranty is built around functionality over time. It is designed to handle the cost of repairing or replacing systems and appliances that fail through normal use.

What’s Usually Included

Most plans cover:

- Heating and cooling systems

- Electrical and plumbing systems

- Kitchen appliances

- Water heaters and similar equipment

For example, if your refrigerator stops cooling or your air conditioning system breaks down during peak summer, a home warranty is intended to address those types of issues.

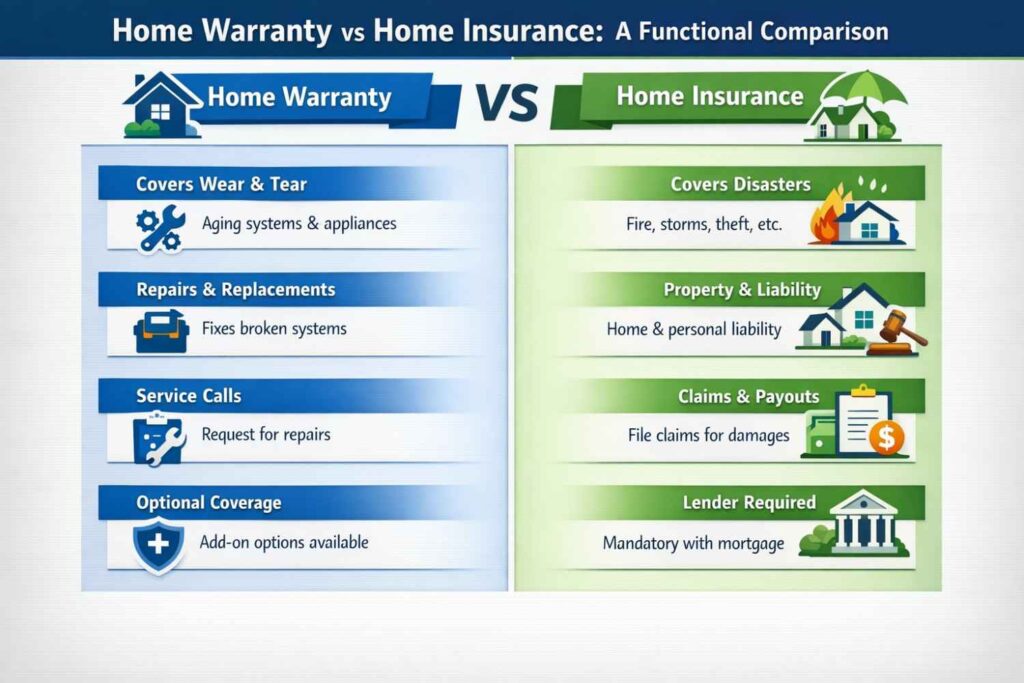

Home Warranty vs Home Insurance: A Functional Comparison

To fully understand home warranty vs home insurance, it helps to look beyond definitions and focus on how they function in real scenarios.

| Situation | Covered By |

|---|---|

| Fire damages part of your home | Home Insurance |

| Storm causes roof damage | Home Insurance |

| Dishwasher stops working | Home Warranty |

| HVAC system fails due to age | Home Warranty |

As a result, the difference is not about better or worse—it’s about which type of problem you are dealing with.

Coverage Boundaries: Why Gaps Happen

One of the most common issues homeowners face is assuming that coverage overlaps more than it actually does.

In reality, there is a clear boundary:

- Insurance handles sudden impact

- Warranty handles gradual failure

However, problems arise in situations that fall somewhere in between.

For example, consider a water heater that fails without any external cause. It’s not damaged by an event, yet it’s also not something you planned for financially. In this case, insurance would not apply. If you don’t have a warranty, the cost becomes entirely out-of-pocket.

Because of this gap, understanding both types of coverage becomes essential rather than optional.

Cost Structure: Why They Feel Different Financially

Another key distinction in the home warranty vs home insurance comparison is how costs are structured.

Home Insurance Costs

Insurance premiums are influenced by multiple variables, including:

- Property value

- Location and environmental risk

- Coverage limits

- Deductible level

As a result, costs can vary significantly. In many cases, homeowners pay anywhere between $1,200 and $2,500 annually, although this range can increase depending on risk exposure.

If you want a more tailored estimate based on your specific property, using an online insurance estimator can provide a clearer picture.

Home Warranty Costs

Home warranties, on the other hand, are more standardized:

- Annual plan cost

- Fixed service fee per repair visit

While the yearly premium is typically lower, each service request involves an additional fee. Therefore, the total cost depends on how frequently repairs are needed.

Because of this structure, warranties are often seen as a way to stabilize smaller, unpredictable expenses, rather than protect against large-scale loss.

When Each Type of Coverage Becomes Essential

Instead of asking which option is better, it’s more useful to ask when each becomes necessary.

Situations Where Home Insurance Is Critical

Home insurance is essential when:

- You want protection against major financial loss

- You own property in areas exposed to weather risks

- You have a mortgage (where it is usually required)

Without it, a single event could result in overwhelming repair costs.

Situations Where a Home Warranty Adds Value

A home warranty becomes useful when:

- Your home systems are aging

- You want predictable repair costs

- You prefer simplified service coordination

For homeowners who want to reduce uncertainty around maintenance expenses, a warranty can provide an added layer of financial predictability.

Also, Most standard policies include structural protection, personal property coverage, and liability protection. However, coverage details can vary depending on the provider and policy structure. For a general explanation of how homeowners insurance works, you can refer to resources provided by the Consumer Financial Protection Bureau.

Why Many Homeowners Misjudge This Decision

Despite the differences, many homeowners misunderstand how these two forms of protection interact.

One common assumption is that insurance will cover everything inside the home. However, that is not the case. Insurance is not designed for maintenance-related issues.

On the other hand, some believe a home warranty offers complete coverage for all repairs. In reality, warranties have limits, exclusions, and specific terms that define what is eligible.

Because of these misunderstandings, coverage gaps often go unnoticed—until a claim is denied.

A More Practical Way to Think About It

Rather than viewing this as a comparison, it helps to think of it as two layers of protection:

- The first layer protects against unexpected events

- The second layer manages ongoing system reliability

When combined, they create a more complete approach to home protection. However, depending on your home’s age and condition, you may not always need both.

Final Thoughts

The conversation around home warranty vs home insurance is often framed as a choice. In reality, it is about understanding how each one fits into a broader strategy.

Home insurance provides protection when something sudden and significant happens. Meanwhile, a home warranty addresses the smaller, inevitable breakdowns that come with time.

By recognizing where each type of coverage applies—and where it doesn’t—you can make decisions that are not only more informed, but also more aligned with how homes actually function over time.

Ultimately, the goal isn’t just to have coverage. It’s to have the right coverage for the situations you’re most likely to face.