If you live in a hurricane-prone area, you’ve probably seen the term “hurricane deductible” on your home insurance policy. However, for many homeowners, it’s not entirely clear what it actually means—or how it affects a claim when a storm hits.

Understanding your hurricane deductible is important because it directly impacts how much you’ll pay out of pocket after a covered loss. And in many cases, it works very differently from a standard deductible.

So, let’s break it down in simple terms and answer the questions homeowners usually have.

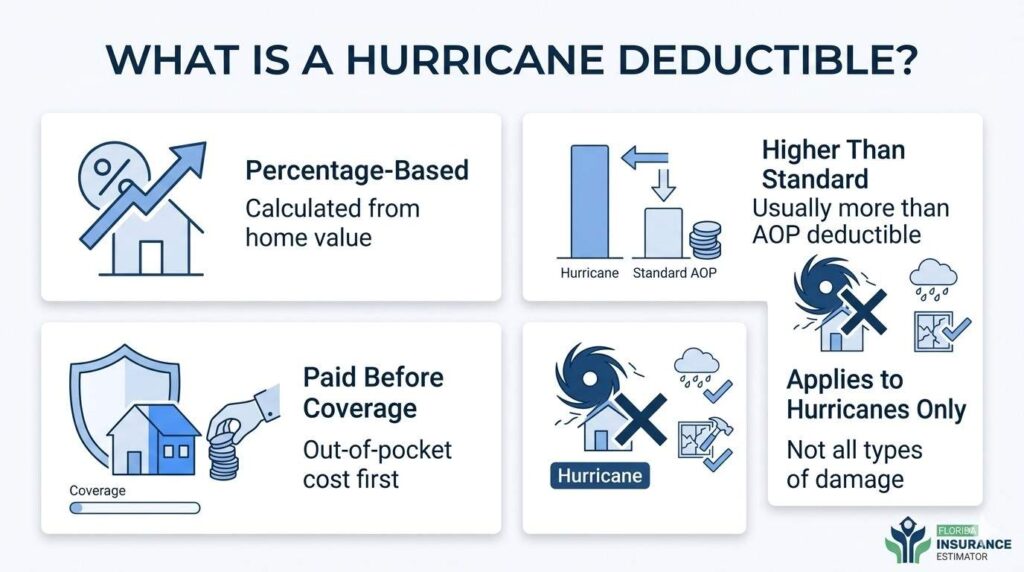

What Is a Hurricane Deductible?

It is the amount you’re responsible for paying before your insurance coverage kicks in for damage caused by a hurricane.

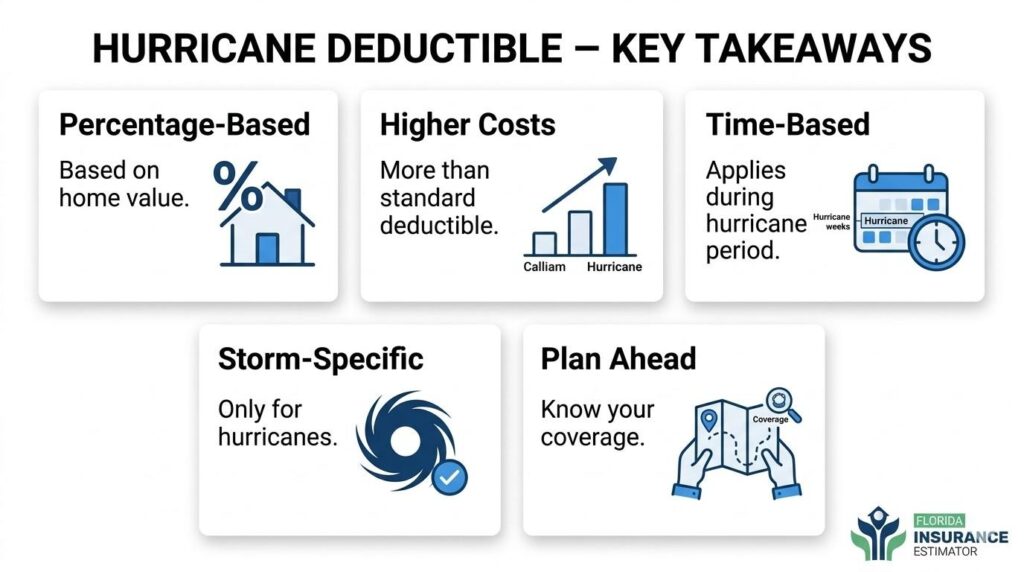

Unlike a standard deductible, which is usually a fixed dollar amount, a hurricane deductible is often calculated as a percentage of your home’s insured value.

For example:

- If your home is insured for $300,000

- And your hurricane deductible is 2%

- You would pay $6,000 out of pocket before insurance covers the rest

Because of this structure, hurricane deductibles are typically higher than standard deductibles.

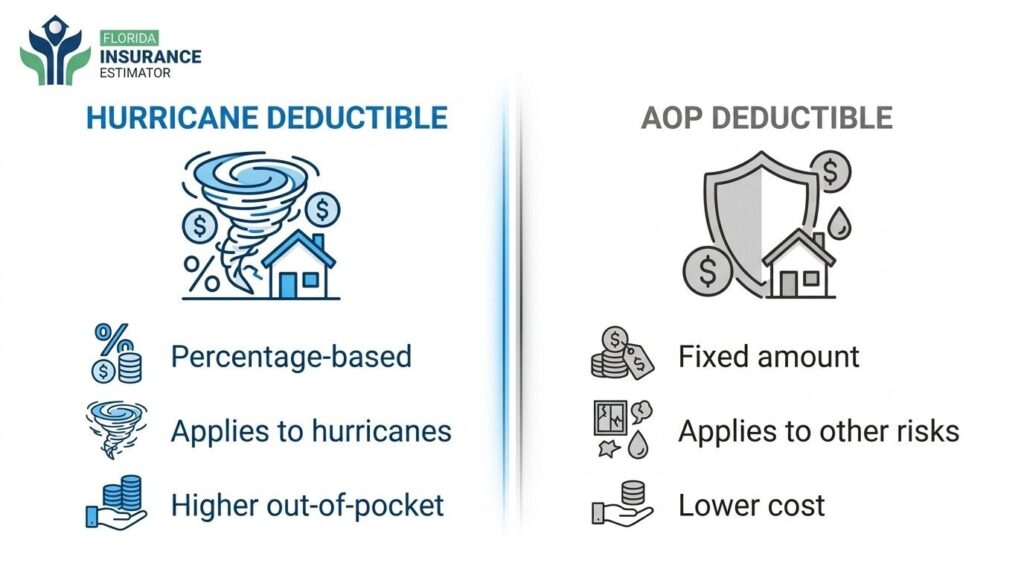

How Is It Different From a Standard (AOP) Deductible?

Most home insurance policies include what’s known as an AOP deductible (All Other Perils deductible). This applies to everyday risks like fire, theft, or minor weather damage.

However, hurricane damage is treated differently.

Key Differences:

- AOP Deductible:

Fixed amount (e.g., $1,000 or $2,500) - Hurricane Deductible:

Percentage-based (e.g., 1%–5% of home value)

This means that in the event of a hurricane, your costs could be significantly higher than for other types of claims.

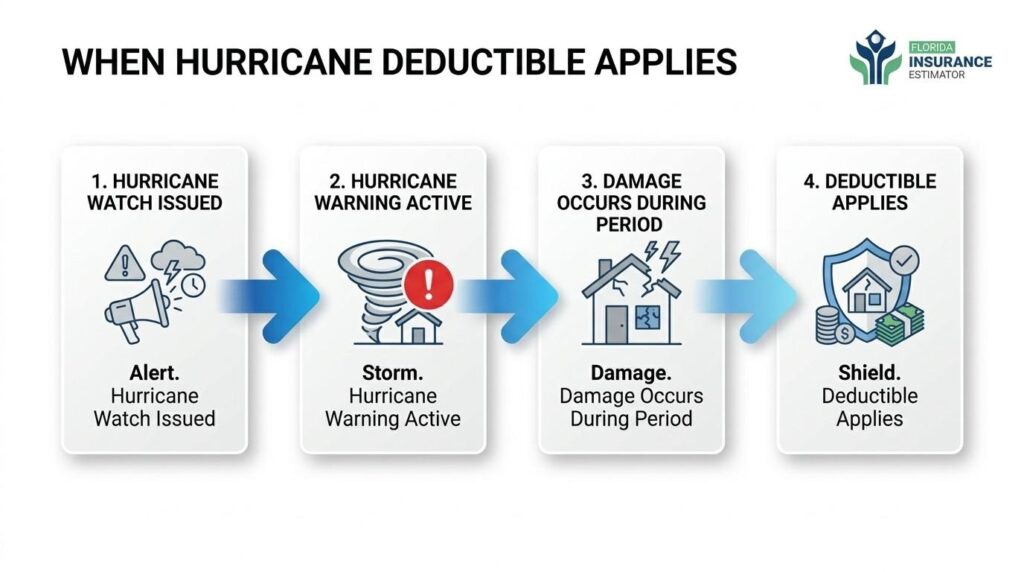

When Does a Hurricane Deductible Apply?

It doesn’t apply to every storm—it only applies under specific conditions.

Typically, it is triggered when:

- A storm is officially classified as a hurricane by the National Weather Service

- The storm affects your area during a defined time period

This is where the concept of a hurricane duration deductible comes in.

What Is a Hurricane Duration Deductible?

A hurricane duration deductible refers to the time window during which your hurricane deductible is active.

Usually, this period:

- Starts when a hurricane watch or warning is officially announced

- Ends a certain number of hours after the warning is lifted

If the damage happens during that period, it will apply. If it happens outside that window, your standard AOP deductible may apply instead.

Because of this, timing can play a major role in how your claim is handled.

Why Do Insurance Companies Use Hurricane Deductibles?

Hurricanes can cause widespread and costly damage. Because of that, insurers use hurricane deductibles to manage risk and keep premiums more affordable overall.

Without them:

- Insurance costs in hurricane-prone areas would likely be much higher

- Coverage might be harder to obtain

While it may seem like an added burden, the structure helps balance risk across policyholders.

How Much Is a Typical Hurricane Deductible?

In most cases, hurricane deductibles fall between 1% and 5% of your home’s insured value

Here’s a quick example:

| Home Value | 2% Deductible | 5% Deductible |

|---|---|---|

| $200,000 | $4,000 | $10,000 |

| $400,000 | $8,000 | $20,000 |

As you can see, even a small percentage can result in a significant out-of-pocket cost.

That’s why it’s important to understand your policy before a storm happens—not after.

What Does a Hurricane Deductible Cover?

A home insurance hurricane deductible applies specifically to damage caused by hurricanes. This can include:

- Wind damage to your home

- Roof damage

- Structural damage

- Damage to attached structures (like garages)

However, not all hurricane-related damage is automatically covered.

For example:

- Flood damage typically requires separate flood insurance

- Some exclusions may apply depending on your policy

So, it’s always a good idea to review your coverage details carefully.

How to Know Your Hurricane Deductible

If you’re unsure about your deductible, you can usually find it in your insurance policy under the deductible section.

Look for:

- Percentage-based deductible details

- Hurricane or named storm deductible clauses

If it’s still unclear, contacting your insurance provider can help clarify things.

Additionally, tools like an insurance estimator can help you understand how different deductibles might affect your potential costs.

Can You Choose Your Hurricane Deductible?

In many cases, yes.

Insurance providers may offer different deductible options, such as:

- 1% (lower out-of-pocket, higher premium)

- 2%–3% (balanced option)

- 5% (higher out-of-pocket, lower premium)

The best option largely comes down to your financial situation and how much risk you’re comfortable taking on

For example:

- If you want lower upfront costs during a claim, a lower deductible may make sense

- If you want to reduce your premium, a higher deductible might be an option

Common Questions Homeowners Ask

A. No. It only applies when a storm is officially classified as a hurricane and meets the policy conditions.

A. In many policies, the hurricane deductible applies once per hurricane season, not per event—but this can vary.

A. If the damage occurs outside the hurricane duration period, your standard deductible may apply instead.

A. Not always. Coverage depends on your policy, and flood damage is usually excluded unless separately insured.

Why Understanding This Matters

Many homeowners only realize how their deductible works when they file a claim. By that point, it can be too late to make adjustments.

Understanding your hurricane deductible ahead of time helps you:

- plan for potential costs

- avoid surprises

- choose the right coverage level

Because hurricanes are unpredictable, being prepared financially can make a big difference.

Final Thoughts

A hurricane deductible is a key part of home insurance in storm-prone areas, yet it’s often misunderstood.

At a glance, it may seem like just another policy detail. However, when a major storm hits, it becomes one of the most important factors in determining how much you’ll pay out of pocket.

The best approach is simple:

- know your percentage

- understand when it applies

- review your coverage regularly

That way, if a hurricane does impact your area, you’re not left figuring things out in the middle of an already stressful situation.