If you’re a homeowner—or planning to become one—you’ve likely come across both mortgages and home equity loans. At first, they might seem similar since both involve borrowing money using a home. However, they serve very different purposes.

Understanding the difference between a home equity loan vs mortgage is important because choosing the wrong option could cost you more in the long run or limit your financial flexibility.

This guide breaks everything down clearly so you can make the right decision based on your situation.

What distinguishes a home equity loan from a mortgage?

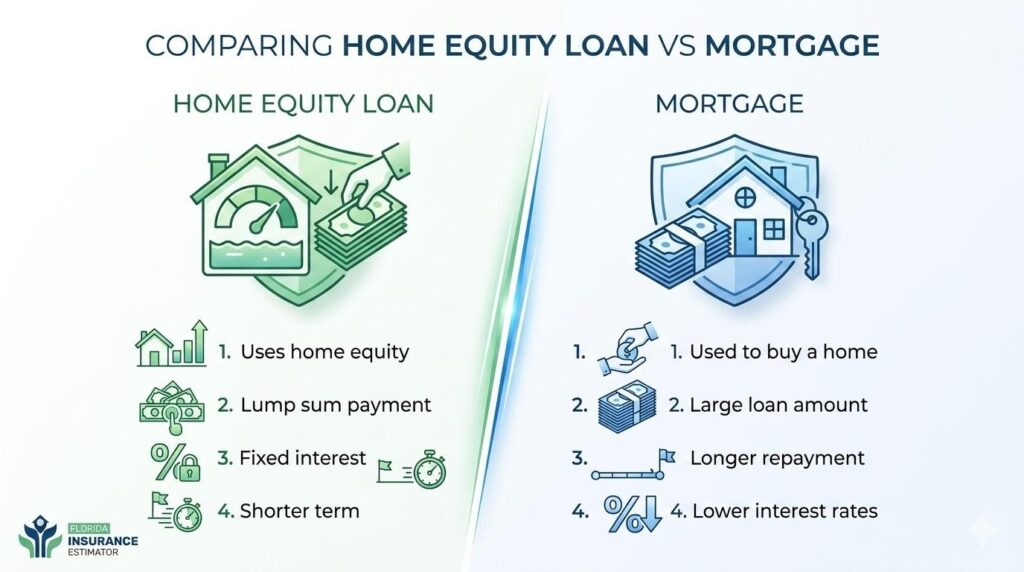

A mortgage is a loan used to buy a home, while a home equity loan allows you to borrow against the value of a home you already own.

In simple terms:

- A mortgage helps you purchase a property

- A home equity loan lets you tap into the equity you’ve accumulated in your property

What Is a Mortgage?

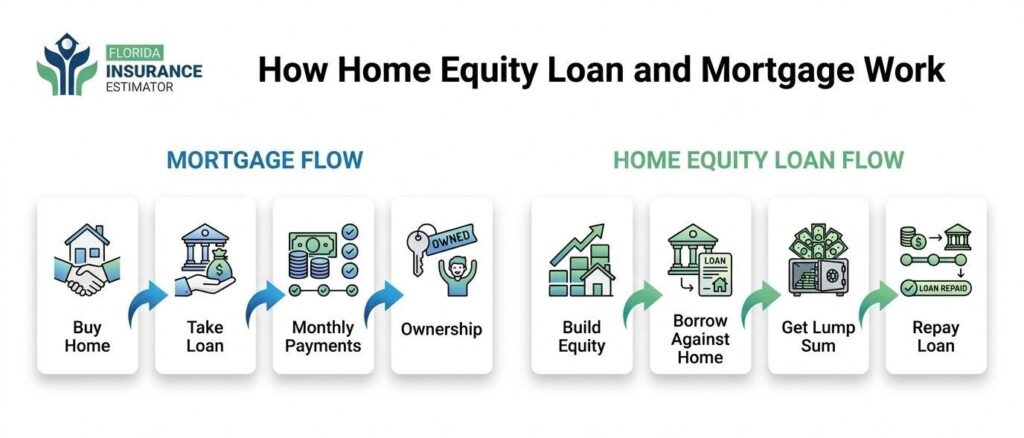

A mortgage is typically the first loan you take when buying a home. It allows you to spread the cost of the property over many years instead of paying everything upfront.

Key Features of a Mortgage:

- Used to buy or refinance a home

- Long repayment terms (usually 15–30 years)

- Interest rates can be fixed or adjustable

- Secured by the property itself

Because mortgages involve large amounts of money, lenders carefully evaluate your credit score, income, and financial history.

What Is a Home Equity Loan?

A home equity loan, commonly referred to as a second mortgage, gives you access to funds using your home’s equity

What Is Home Equity?

Home equity is the difference between:

What your home is worth

What you still owe on your mortgage

For example:

- Home value: $400,000

- Remaining mortgage: $250,000

Equity: $150,000

Key Features of a Home Equity Loan:

- Borrow against existing home equity

- Usually comes with a fixed interest rate

- Paid in a lump sum

- Typically shorter terms (5–20 years)

Because of this, it’s often used for:

- Home improvements

- Debt consolidation

- Major expenses

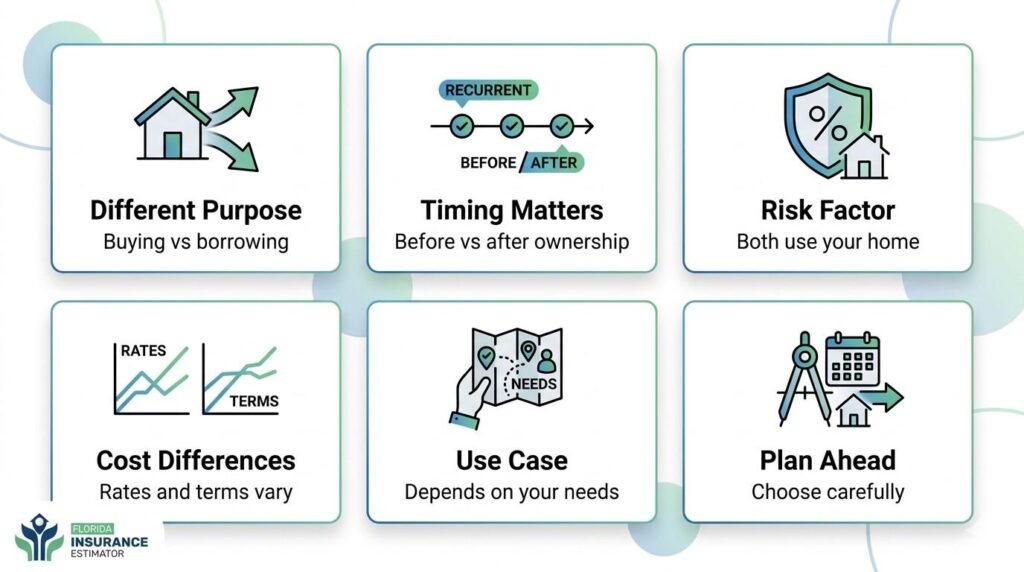

Home Equity Loan vs Mortgage: Key Differences

Understanding the differences helps you decide which option fits your needs.

Purpose

- Mortgage: Used to buy or refinance a home

- Home Equity Loan: Used to access cash from your home’s value

Timing

- Mortgage: Taken when purchasing a home

- Home Equity Loan: Taken after you’ve built equity

Loan Structure

- Mortgage: Large loan, long-term repayment

- Home Equity Loan: Smaller loan, shorter repayment

Interest Rates

- Mortgages often have lower rates

- Home equity loans may have slightly higher rates but are usually fixed

Risk

Both are secured loans, meaning:

Your home is used as collateral

However, taking on additional loans increases your financial risk if you’re unable to repay.

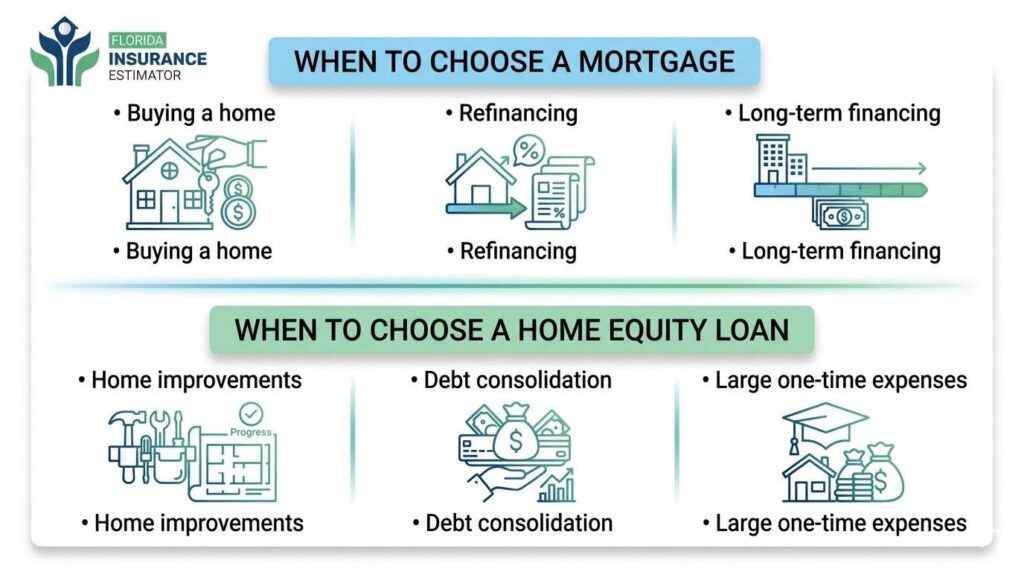

When Should You Choose a Mortgage?

A mortgage is the right option if:

- You’re buying a home

- You’re refinancing to get a better rate

- You want to change loan terms

In most cases, you don’t have a choice here—if you’re purchasing property, you’ll need a mortgage unless you’re paying in cash.

When Should You Choose a Home Equity Loan?

A home equity loan makes more sense when:

- You’ve built sufficient equity

- You’re looking for a single payout to cover a specific cost

- You want predictable monthly payments

It’s commonly used for projects like:

- Renovating your home

- Covering large medical expenses

- Consolidating high-interest debt

Pros and Cons of Each Option

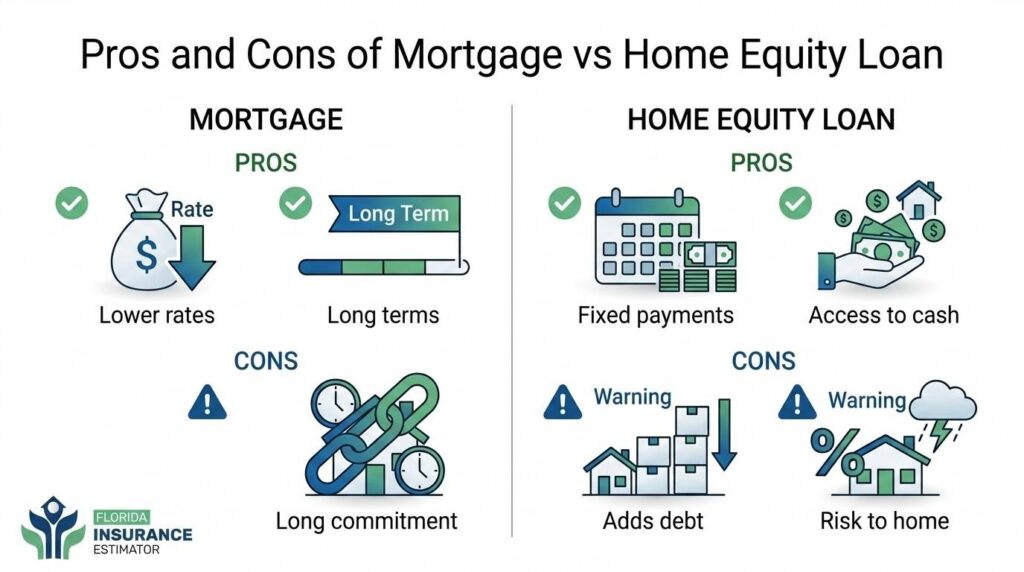

Mortgage Pros:

- Lower interest rates

- Longer repayment periods

- Essential for homeownership

Mortgage Cons:

- Long-term financial commitment

- Interest paid over time can be significant

Home Equity Loan Pros:

- Access to large amounts of cash

- Fixed interest rates

- Useful for planned expenses

Home Equity Loan Cons:

- Adds another monthly payment

- Risk of foreclosure if not repaid

- Reduces available equity

Can You Have Both at the Same Time?

Yes, many homeowners have both a mortgage and a home equity loan.

In this case:

- The mortgage is the primary loan

- The home equity loan is the secondary loan

However, lenders will consider your total debt and income before approving a second loan.

What About HELOC vs Home Equity Loan?

While comparing home equity loan vs mortgage, it’s also worth mentioning HELOCs (Home Equity Lines of Credit).

- Home Equity Loan: Lump sum, fixed rate

- HELOC: Revolving credit, variable rate

HELOCs offer flexibility, but they come with variable interest rates, which can change over time.

How Do You Decide Which One Is Right for You?

The right choice depends on your situation.

Choose a Mortgage If:

- You’re buying a home

- You need long-term financing

- You want lower interest rates

Choose a Home Equity Loan If:

- You already own a home

- You need a specific amount of money

- You want fixed, predictable payments

Factors to Consider Before Deciding

Before choosing between a home equity loan vs mortgage, consider:

- Your current financial stability

- How much equity you have

- Interest rates and loan terms

- Your long-term financial goals

It’s also helpful to estimate your overall home-related costs. For example, tools like a fl insurance calculator can help you understand how insurance expenses fit into your budget alongside loan payments.

Common Questions Homeowners Ask

A. Not necessarily. They serve different purposes. One isn’t better—it depends on your needs.

A. Yes, but it’s less common and comes with additional risk.

A. No. It’s a separate loan in addition to your mortgage.

A. Mortgages generally have lower rates, especially primary mortgages.

Final Thoughts

When comparing a home equity loan vs mortgage, the key difference comes down to timing and purpose.

A mortgage helps you buy a home, while a home equity loan helps you make use of the value you’ve already built. Both can be useful tools when used correctly, but they also come with responsibilities.

The best approach is to understand your financial position, consider your goals, and choose the option that aligns with your needs—not just what seems easiest in the moment.