When most people think about home insurance, they focus on protecting the house itself. However, one of the most important parts of a policy often gets overlooked liability coverage. So, what exactly does it do? Understanding home insurance liability coverage can help you avoid serious financial risks. More importantly, it gives you peace of mind knowing you’re protected if something unexpected happens.

What Is Home Insurance Liability Coverage? (Quick Answer)

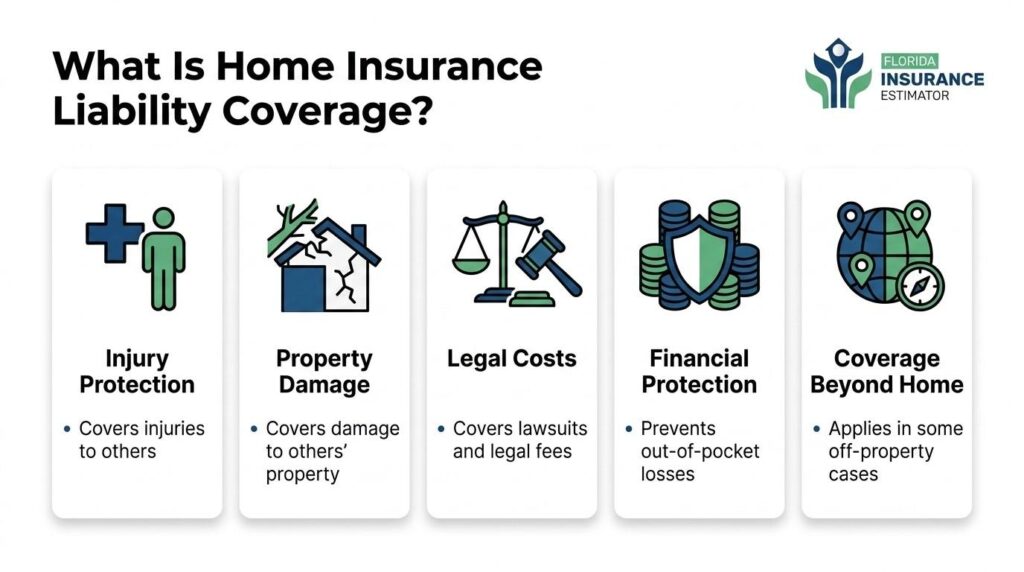

Home insurance liability coverage protects you financially if someone is injured or their property is damaged and you’re legally responsible.

In other words, it helps cover:

- medical expenses

- legal fees

- settlement or court costs

Because of this, it acts as a financial safety net for situations that could otherwise become very expensive.

What Does Liability Insurance Cover?

One of the most common questions homeowners ask is: what does liability insurance cover?

While coverage can vary slightly depending on the policy, most standard plans include the following:

Bodily Injury to Others

If an injury occurs on your property, your liability coverage may help pay for:

- medical bills

- hospital visits

- rehabilitation costs

For example, if a guest slips on your driveway and gets injured, your policy may cover the related expenses.

Property Damage

If you accidentally damage someone else’s property, your policy may cover repair or replacement costs.

For instance:

- your child breaks a neighbor’s window

- your dog damages someone’s belongings

In these situations, liability coverage can step in.

Legal Costs

If a claim turns into a lawsuit, legal expenses can quickly add up.

Liability coverage typically includes:

- attorney fees

- court costs

- settlements or judgments

This is one of the most valuable aspects of personal liability coverage in home insurance, since legal fees alone can be significant.

Incidents Away From Home

Many homeowners don’t realize that liability coverage often extends beyond their property.

For example:

- your dog bites someone at a park

- you accidentally cause damage while visiting someone

In many cases, your policy still provides protection.

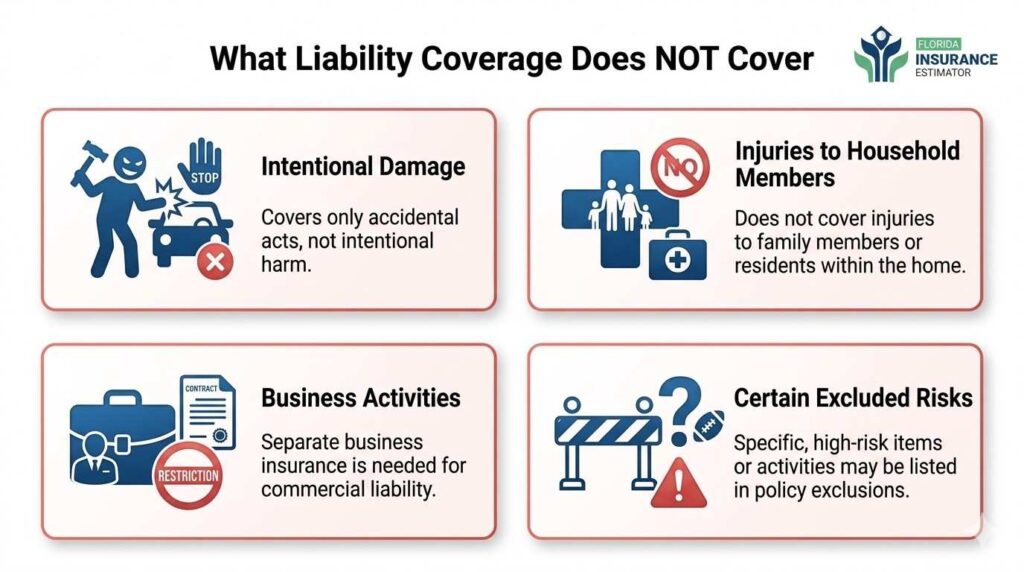

What Liability Coverage Does NOT Cover

While liability coverage is broad, it does have limits.

Typically, it does not cover:

- intentional damage or harm

- injuries to household members

- business-related activities (unless specifically added)

- damage covered under other sections of your policy

Because of this, it’s important to review your policy carefully to understand what’s included and what isn’t.

How Home Insurance Liability Coverage Works

Understanding how it works in real situations can make things clearer.

Let’s say someone files a claim against you. Here’s what usually happens:

- The incident is reported to your insurance provider

- The insurer investigates the claim

- If you’re found responsible, coverage applies

- The insurer pays for eligible expenses up to your policy limit

As a result, you’re not left paying out of pocket for large, unexpected costs—at least within your coverage limits.

How Much Liability Coverage Do You Need?

For homeowners, this is an important choice to think through carefully

Most policies start with limits like:

- $100,000

- $300,000

However, many experts recommend higher coverage, especially if you:

- own valuable assets

- have savings or investments

- host guests frequently

Simply put, if a claim goes beyond your coverage limit, you’ll be responsible for paying the remaining amount

What Are Liability Limits?

Your home insurance liability limits refer to the maximum amount your policy will pay for a covered claim.

For example:

- If your limit is $300,000

- And a claim costs $350,000

You may be responsible for the remaining $50,000

Because of this, choosing the right limit is just as important as having coverage in the first place.

Why Liability Coverage Matters More Than You Think

At first glance, liability coverage might not seem as important as protecting your home itself. However, in many cases, it’s just as critical—if not more.

Here’s why:

Financial Protection

Unexpected incidents can lead to large expenses. Without proper coverage, you’ll need to handle those costs on your own.

Legal Protection

Even a simple claim can turn into a legal case. Liability coverage helps manage those costs.

Everyday Risks

Accidents happen more often than people expect. From minor injuries to property damage, risks exist in everyday situations.

Common Situations Where Liability Coverage Applies

To better understand its value, here are some real-world examples:

- A guest falls and gets injured at your home

- Your dog bites a visitor

- Your child damages a neighbor’s property

- Someone files a claim after an accident involving your actions

In each case, liability coverage can help protect you financially.

How Liability Coverage Fits Into Your Overall Policy

A homeowners insurance policy usually includes several parts:

- dwelling coverage (protects your home)

- personal property coverage (protects belongings)

- liability coverage (protects you financially)

Each part plays a different role, but together they provide complete protection.

Factors That Affect Liability Coverage Needs

Not every homeowner needs the same level of coverage. Several factors can influence your decision:

- number of visitors or guests

- presence of pets

- property features (like pools or trampolines)

- personal assets and financial situation

Because of these variables, it’s important to evaluate your risks carefully.

How to Choose the Right Liability Coverage

Finding the right coverage can be straightforward with the right approach. However, it does require some planning.

Assess Your Risk

Think about your lifestyle and property. Do you host gatherings often? Do you have features that could increase risk?

Consider Your Assets

Higher assets often mean a greater need for financial protection.

Review Policy Options

Different policies offer different limits and features. Take time to compare them.

Use Estimation Tools

Tools like an insurance calculator can help you get a better idea of coverage needs and potential costs based on your situation.

Common Questions About Home Insurance Liability Coverage

A. It’s not always legally required, but it’s strongly recommended due to the financial risks involved.

A. Yes, most policies include a separate section for minor medical expenses, regardless of fault.

A. Yes, you can usually increase your limits or add umbrella coverage for additional protection.

A. Yes, it typically covers legal defense costs and settlements up to your policy limits.

Also, You can also check this guide on how much home insurance costs in 2026 to better understand the pricing factors that shape your overall coverage.

Final Thoughts

Understanding home insurance liability coverage is essential for protecting more than just your property—it protects your financial future.

While it may not always be the most visible part of your policy, it plays a critical role when unexpected situations arise. From covering medical expenses to handling legal costs, liability coverage helps you manage risks that could otherwise be overwhelming.

Ultimately, the goal isn’t just to have coverage—it’s to have the right coverage based on your needs. Taking the time to understand your options now can save you from major stress later.