Flooding ranks as one of the most common and costly natural disasters in the United States. Yet, many homeowners are still unsure about how flood insurance works—or more importantly, how much it actually costs.

So, how much is flood insurance in 2026?

The answer isn’t one-size-fits-all. Instead, flood insurance costs depend on several factors, including your location, property details, and level of risk. Because of this, two homes in the same city can have very different premiums.

In this guide, we’ll break down average costs, explain what affects pricing, and help you understand what to expect before purchasing a policy.

How Much Is Flood Insurance? (Quick Answer)

On average, flood insurance in the U.S. costs between $700 and $1,500 per year. However, in higher-risk areas, premiums can exceed $2,000 annually.

At the same time, some lower-risk properties may pay significantly less.

Because of these variations, it’s important to look beyond averages and understand what drives the cost.

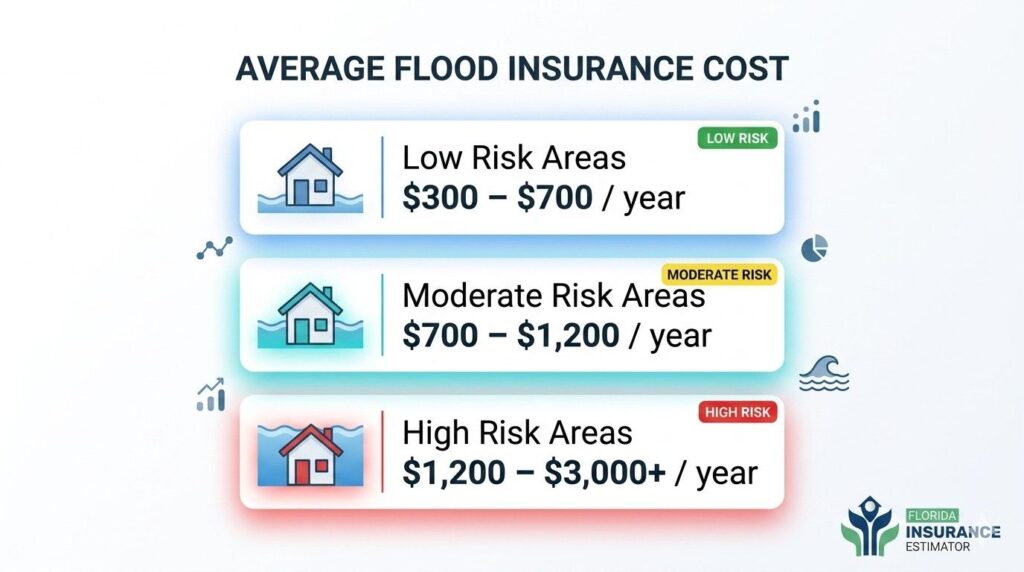

Average Flood Insurance Cost in the U.S.

To help you better understand, here’s a general breakdown:

- Low-risk areas: $300 – $700 per year

- Moderate-risk areas: $700 – $1,200 per year

- High-risk areas: $1,200 – $3,000+ per year

While these ranges provide a useful starting point, they don’t reflect individual property differences. Therefore, your actual premium may fall outside these estimates.

What Affects Flood Insurance Costs?

The pricing is based on risk. The higher the risk of flooding, the higher the premium.

However, several specific factors determine your final cost.

Flood Zone Classification

Your property’s flood zone is one of the biggest pricing factors.

- High-risk zones (e.g., FEMA Special Flood Hazard Areas): Higher premiums

- Moderate-to-low-risk zones: Lower premiums

Because of this, two homes with similar features can have very different costs based on location alone.

Elevation and Property Height

Homes built above the base flood elevation generally cost less to insure.

On the other hand, properties below expected flood levels face higher premiums.

Home Value and Structure

The size and value of your home also impact cost.

For example:

- Larger homes typically cost more to insure

- Construction materials can affect risk levels

Coverage Amount

The amount of coverage you select will directly influence how much you pay.

insurance policies typically include:

- building coverage

- personal property coverage

Adjusting these limits can significantly change your annual cost.

Deductible

Your deductible plays a direct role in pricing.

- Higher deductible → Lower premium

- Lower deductible → Higher premium

Therefore, choosing the right deductible requires balancing affordability and risk.

Age and Design of the Home

Older homes, especially those not built with modern flood standards, may cost more to insure.

Meanwhile, newer homes with flood-resistant features often receive better rates.

Type of Flood Insurance Policy

There are two main types of policies:

FEMA (NFIP) Policies

- Backed by the federal government

- Standardized coverage

Private Flood Insurance

- Offered by private insurers

- More flexible coverage options

In some cases, private policies may offer lower rates or higher coverage limits.

FEMA Flood Insurance Cost (NFIP)

The National Flood Insurance Program (NFIP) is one of the most common options.

On average:

- NFIP policies cost around $800 to $1,200 per year

However, recent changes like FEMA’s Risk Rating 2.0 have shifted pricing to better reflect individual property risk.

As a result:

- some homeowners pay less

- others may see higher premiums

Can Flood Insurance Be Cheaper?

Yes, in some cases, insurance can be more affordable than expected.

For example:

- homes in low-risk zones often qualify for lower rates

- higher deductibles can reduce premiums

- mitigation features (like elevation or drainage improvements) may lower costs

However, even if your area isn’t considered high risk, flooding can still happen. Because of this, many homeowners choose coverage for added protection.

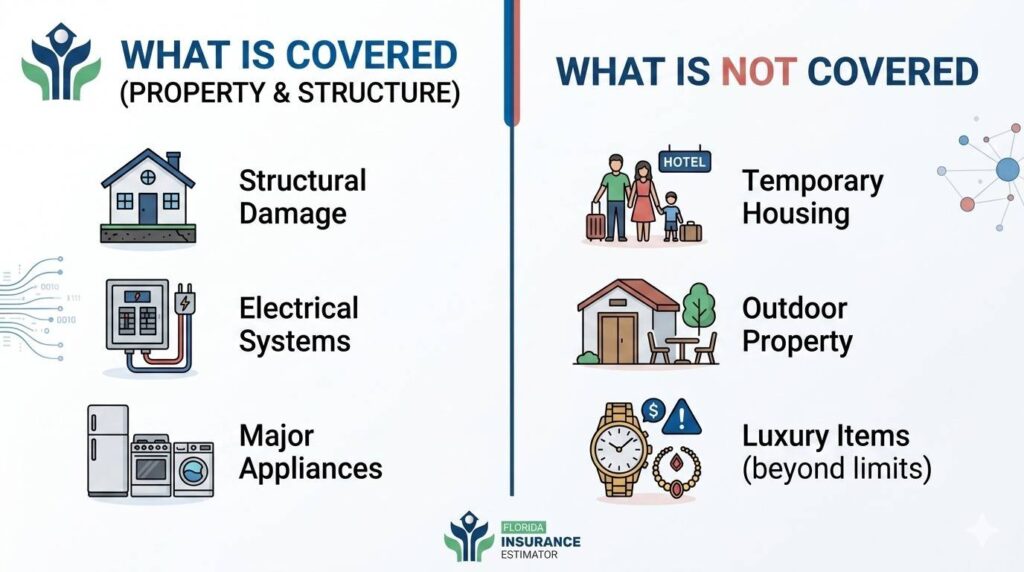

What Flood Insurance Typically Covers

Understanding coverage is just as important as understanding cost.

Covered:

- structural damage to your home

- electrical and plumbing systems

- major appliances

- flooring and built-in features

Personal Property (Optional Coverage):

- furniture

- electronics

- clothing

Not Covered:

- temporary housing

- outdoor property (like landscaping)

- certain valuables beyond limits

Because of these limits, some homeowners choose additional coverage options.

Waiting Period for Flood Insurance

One important detail many people overlook is the waiting period.

Most flood insurance policies have a:

30-day waiting period before coverage begins

However, there are exceptions in certain situations, such as mortgage requirements.

Is Flood Insurance Required?

It is not required for every homeowner.

However, it becomes mandatory if:

- your home is in a high-risk flood zone

- you have a federally backed mortgage

Even if it’s not required, many homeowners still choose coverage due to the financial risks of flooding.

Is Flood Insurance Worth It?

This is a common question, and the answer ultimately depends on your specific situation.

It may be worth it if:

- you live in a flood-prone area

- your home is near water

- you want financial protection from unexpected damage

It may be less urgent if:

- your property is in a low-risk zone

- you’re willing to accept potential out-of-pocket risk

However, it’s important to remember that flooding can occur outside high-risk zones as well.

How to Estimate Your Flood Insurance Cost

Because prices vary widely, it’s helpful to estimate your potential cost before purchasing a policy.

You can do this by:

- checking your flood zone

- reviewing your home’s elevation

- comparing coverage options

Additionally, using tools like an insurance estimator can help you better understand how different factors influence your expected premium.

Flood Insurance Costs by Location

Location plays a major role in determining cost.

For example:

- coastal states like Florida and Louisiana often have higher premiums

- inland areas may see lower costs

Even within the same state, prices can vary based on local flood risk.

How Flood Insurance Is Changing

The pricing has evolved in recent years.

With updates like FEMA’s Risk Rating 2.0:

- premiums are now more personalized

- property-specific risk plays a bigger role

- pricing reflects real flood exposure more accurately

As a result, homeowners now receive more tailored pricing—but also need to pay closer attention to their risk factors.

Common Questions About Flood Insurance Costs

A. On average, costs range from $60 to $125 per month, depending on risk level.

A. Because it’s based on risk. Areas with higher flood probability require higher premiums to cover potential losses.

A. Yes. You can reduce costs by:

– increasing your deductible

– improving flood protection features

– choosing appropriate coverage levels

A. Not necessarily, but it’s still worth considering. Many flood claims come from outside high-risk zones.

What to Expect When Buying Flood Insurance

When purchasing a policy, you can expect:

- A review of your property’s flood risk

- A quote based on your coverage choices

- A waiting period before coverage starts

- Annual renewal with updated pricing

Because of this process, it’s helpful to plan ahead rather than waiting until the last minute.

Final Thoughts

So, how much is flood insurance?

While average costs provide a general idea, the actual price depends on your property, location, and coverage choices. Because of this, understanding the factors behind pricing is just as important as knowing the numbers.

Ultimately, it is about managing risk. Whether you live in a high-risk area or not, having the right coverage can protect you from significant financial loss.

By taking the time to understand your options and estimate your costs, you can make a more informed decision—and avoid unexpected surprises later.